Let’s face it. There is big elephant in the room when it comes to achieving financial independence.

The elephant is this: There are systems we rely on to get to financial independence which are subject to forces outside our control.

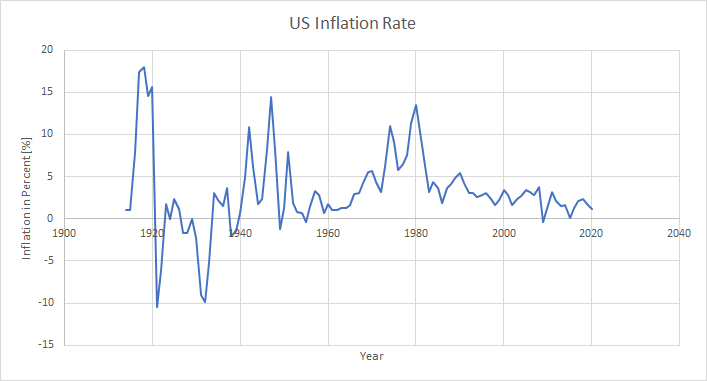

One of the biggest of these is inflation. Inflation is defined by the increase in goods price. The FED measures this with the Consumer Price Index. However, this index can be quite wrong. In fact last year (2020) the feds printed so much money there was 20% dollars going around than in 2019. However, the CPI just maintained the same 2%.

Sound fishy? Yes, you would be right.

The Fed shoots for 2% year after year because they believe that it will stimulate the economy long term.

However, the money printing we saw will have an effect on inflation. It should be noted that money printing doesn’t necessarily mean inflation. That is because just because more dollars are going around more people will spend that (demand) or that goods are being produced more (supply). It also doesn’t mean that US consumers are using those dollars. If a foreign central bank holds those dollars or treasuries, then they might not necessarily play into our market, essentially hiding those dollars from the market. However, despite what the CPI says, many markets are seeing high inflation in goods prices, particularly in steel.

Okay, now we have that cleared up. We know know intuitively that an increase in inflation can cause issues with cost of living in future years, essentially making the 9% average growth of you VTSAX be lower.

This has a tremendous effect on your portfolio. Say you saved $30k per year for 20 years. You would get $1,672,935. If the Fed gets 2% inflation year after year, that money is worth $1,315,955 in today’s dollars.

However, say we have the same inflation that happened between ’75 and ’80. If that happened on the first 6 years of investing, the same portfolio would be $1,196,982. If that same period happened on the later end of the investing period, the investment would only be $874,443.

That is a $322,539 difference! That would certainly change the landscape of one’s early retirement.

However, there is a way to hedge against this. The method is using leveraged real estate. With leveraged real estate the inflation that is normally working against you is actually working for you.

Say you own a $500k duplex that is a 20% equity. As the inflation goes up, most goods and services also follow as well as the dollar losing value. As inflation ratchets those up, rents increase to follow.

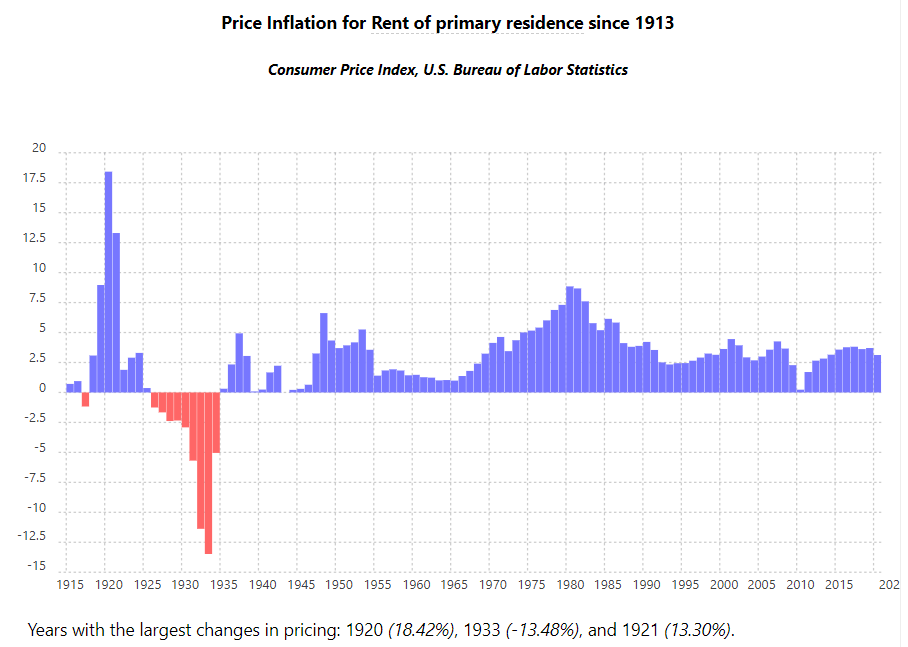

During the high inflation of the late 70s and early 80s, the rents grew dramatically. So relative to the initial purchasing of the property the income is now higher. Between 1975 and 1980, the rent would have risen 39.51%! That is staggering. The ratio of rent income to mortgage interest rises dramatically, increasing cash flow.

There is another benefit, the value of the mortgage will go down with inflation. The dollars that you owe on the property will go down by the same value inflation grows each year. That is good, because you will effectively owe less on the property and the income you produce will be effectively the same, thus increasing your equity faster. Between 1975 and 1980, the “value” of the property went up 60% making your property worth $640k.

Your equity in the property went from 20% to 50% in just 5 years! Crazy.

Now, you may have noticed the period starting in 1929. Yes, that was a tough time where rents down and there was some deflation.

Some say that the dollar and sovereign debt crisis will cause both deflation and lower rental rates. However, we do not know. The real estate industry has had a pretty good run since 1935.

So, if you think there will be inflation and rising rental rates, now might be a good time to invest into real estate, especially when rates are near or below inflation.